Air pollution in major Indian cities has become a global news topic. Particularly, when winter arrives Delhi’s Air Quality Index (AQI) crosses all WHO safe limits, forcing thousands of households to scramble for a solution they could plug into the wall. Traffic is curtailed; schools are shut; and construction is banned.

And yet, many urban households faced an uncomfortable reality: indoor air is often just as polluted as the environment outside. Cooking smoke, poor ventilation, volatile organic compounds, and the constant inflow of PM2.5 particles turned homes into concentrated pollution zones.

Scale of India’s Air Quality Problem

India’s air pollution crisis is structural rather than seasonal, although winter conditions intensify its impact. Northern India regularly records AQI levels in the ‘very poor’ and ‘severe’ categories due to vehicular emissions, industrial activity, construction dust, and agricultural residue burning. Cities such as Delhi, Noida, Ghaziabad, and Lucknow repeatedly suffer AQI levels above 350 during peak winter periods. Western regions across Maharashtra and Gujarat also face poor air quality periodically, while southern cities such as Bengaluru and Chennai continue to exceed safe pollution thresholds despite relatively better environmental conditions.

The health consequences of this severe air pollution are substantial. Exposure to PM2.5 contributes to nearly 2 million premature deaths annually in India. Between 2022 and 2024, over 200,000 cases of acute respiratory illness were recorded across six government hospitals in Delhi, with a significant percentage requiring hospitalization.

Indoor air quality often compounds the problem. Pollutants from cooking, paints, dust, and outdoor infiltration accumulate in poorly ventilated apartments, causing indoor air pollution levels to become two to five times worse than outdoor conditions during severe pollution episodes. As a result, air purifiers are increasingly being viewed as preventive healthcare appliances rather than luxury goods.

Market Driven by Seasonal Demand

India’s air purifier market remains highly seasonal and geographically concentrated. More than 85% of annual sales occur between October and January, directly aligning with North India’s winter pollution cycle. The Delhi-NCR region alone contributes nearly 70% of national demand. Each escalation under the Commission for Air Quality Management’s GRAP framework triggers a spike in purifier sales, online searches, and retail demand. School closures, vehicle restrictions, and media coverage of hazardous AQI levels further intensify consumer urgency.

During winter, air purifiers sales boomed with online search volumes for “best air purifier under ₹5,000” spiked overnight. That paradox sits at the heart of a fast-growing but still a under-leveraged market. According to a report by MarkNtel Advisors, India’s air purifier industry, valued at approximately $63 million (₹567 crore) in 2025, is projected to double to $120 million (₹1140 crore) by 2032, growing at a CAGR of 11.34%. The question is no longer whether Indians need cleaner indoor air. The question is whether the industry, particularly the low-cost segment, can reach all the millions of customers who need it.

Despite rising awareness, overall market penetration remains extremely low compared to India’s population size. Even with increasing sales, the total installed base still covers only a fraction of urban households exposed to unsafe air quality. This reveals a critical gap: Indian consumers understand the dangers of polluted indoor air, but affordability continues to restrict adoption beyond higher-income households.

Low-Cost Gap and Maintenance Challenge

The biggest obstacle for India’s affordable air purifier segment is not simply the purchase price. It is the long-term cost of ownership. Most HEPA-based purifiers require filter replacement once or twice every year to maintain performance. Activated carbon filters, which remove smoke, gases, and VOCs, often require more frequent replacement. Since these devices are used for long hours during pollution seasons, electricity costs also add to the operational burden.

For most consumers, these recurring expenses create hesitation even after the initial purchase. Buyers searching for air purifiers below ₹5,000 often focus on affordability upfront but later discover that filter replacements and maintenance costs significantly increase their annual spending. This challenge has forced manufacturers to rethink their design strategies. Companies targeting the affordable segments are increasingly exploring options such as:

- Washable pre-filters to extend HEPA lifespan

- Longer-life filter materials

- Energy-efficient operating systems

- Compact devices for smaller urban rooms

- Subscription-based filter replacement models

The future of the low-cost air purifier market in India will depend less on reducing retail prices and more on lowering annual maintenance expenses.

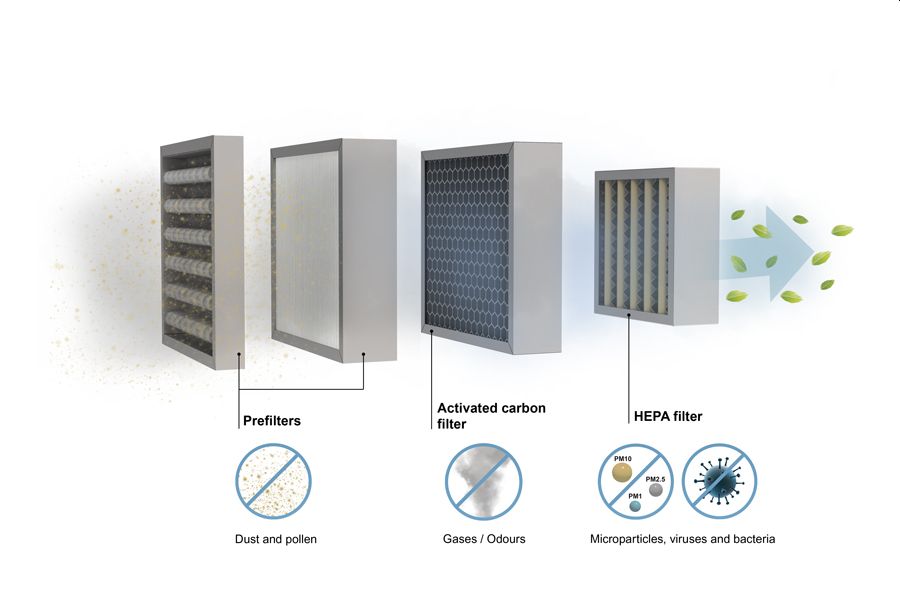

HEPA Dominates the Market

HEPA filtration remains the dominant technology India’s air purifier market, because it directly addresses the country’s most dangerous pollutants: PM2.5 and PM10 particles. The most successful systems combine three layers:

- Pre-filters for larger dust particles

- HEPA filters for particulate removal

- Activated carbon filters for smoke, odors, and VOCs

This combination balances purification efficiency with relatively manageable manufacturing costs. More advanced technologies such as ionizers, UV sterilization, and electrostatic precipitation continue to remain concentrated within premium devices priced above the mass-market segment. While these features are marketed as technological upgrades, they also increase device costs and, in some cases, raise concerns around ozone generation or maintenance complexity.

As a result, India’s price-sensitive market continues to favor practical HEPA-based systems over expensive multi-technology alternatives.

Smart Connectivity Is a Major Trend

One of the most significant developments in India’s air purifier industry is the rise of smart devices. Premium models launched in recent years increasingly include features such as:

- Real-time PM2.5 monitoring

- App-based air quality tracking

- Adaptive fan-speed control

- Wi-Fi and Bluetooth integration

- Voice assistant compatibility

- Filter replacement alerts

These technologies make indoor air pollution visible to consumers. Real-time AQI displays help users understand how polluted their homes actually are and encourage more consistent purifier usage.

Smart functionality is gradually moving into mid-range products as component costs decline. Features once limited to premium devices are becoming more accessible across broader price categories. This transition is important because many Indian consumers purchase air purifiers reactively during pollution emergencies and reduce usage later. Smart monitoring systems may help transform seasonal panic buying into long-term health-focused adoption.

Policy and Regional Expansion Will Shape Growth

Government air-quality initiatives have also become indirect growth drivers for the air purifier market. India’s National Clean Air Programme continues to target reductions in particulate pollution across multiple cities through stricter regulations and expanded monitoring infrastructure. Meanwhile, Delhi’s Winter Action Plans and revised GRAP frameworks have significantly increased public awareness of air pollution risks.

Each policy escalation reinforces the perception that pollution is structural, sustaining consumer demand for indoor purification systems. At the same time, future market growth will increasingly depend on regions outside Delhi-NCR. Western cities such as Mumbai, Pune, and Ahmedabad are witnessing rising adoption due to worsening AQI levels and growing middle-class health awareness. Southern cities including Bengaluru and Chennai are also emerging as important markets, particularly within corporate offices, educational institutions, and healthcare facilities. If these regions begin approaching Delhi’s adoption rates, India’s purifier installed base could expand significantly during the next decade.

The Path Forward

India’s indoor air quality crisis is unlikely to disappear soon. Urbanization, industrial growth, traffic congestion, agricultural burning, and coal dependency will continue keeping pollution levels elevated across regions. The projected 11.34% CAGR in market growth reflects strong underlying demand, but the market’s true opportunity remains largely untapped. The next stage of growth will depend on whether manufacturers can create products that are affordable to purchase and economical to maintain over time. Consumers increasingly understand the health risks associated with indoor air pollution. What the market still lacks is an affordable, transparent, and reliable purifier that remains practical for households even when pollution headlines fade from public attention.

Author bio – Shammi Thakur is a Research Director at MarkNtel Advisors with 15+ years of experience in strategic market intelligence, industry forecasting, and competitive analytics.

{kind=link}